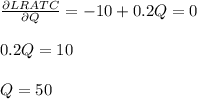

A perfectly competitive industry consists of many identical firms, each with a long-run average total cost of LATC = 800 – 10Q + 0.1Q2 and long-run marginal cost of LMC = 800 – 20Q + 0.3Q2. In long-run equilibrium, each firm produces a quantity of . 50 40 30 60

Answers: 2

Another question on Business

Business, 21.06.2019 22:20

Suppose a ceiling fan manufacturer has the total cost function c(x) = 48x + 1485 and the total revenue function r(x) = 75x. (a) what is the equation of the profit function p(x) for this commodity? p(x) = (b) what is the profit on 35 units? p(35) = interpret your result. the total costs are less than the revenue. the total costs are more than the revenue. the total costs are exactly the same as the revenue. (c) how many fans must be sold to avoid losing money? fans

Answers: 1

Business, 22.06.2019 00:00

If his parents cannot alex with college, and two of his scholarships will be awarded to other students if he does not accept them immediately, which is the best option for him?

Answers: 1

Business, 23.06.2019 08:00

If consumers start to believe they need a product, what is likely to happen? a. the demand becomes less elastic. b. the demand becomes more elastic. c. the supply decreases. d. the price decreases.

Answers: 1

Business, 23.06.2019 11:20

What term refers to searching for potential buyersa. follow up b. presentation c. prospecting d. approach this is on apex learning, principles of business, marketing, and financequiz 4.2.2

Answers: 1

You know the right answer?

A perfectly competitive industry consists of many identical firms, each with a long-run average tota...

Questions

Mathematics, 10.10.2019 13:30

History, 10.10.2019 13:30

Chemistry, 10.10.2019 13:30

Computers and Technology, 10.10.2019 13:30

Mathematics, 10.10.2019 13:30

Biology, 10.10.2019 13:30

Chemistry, 10.10.2019 13:30

Computers and Technology, 10.10.2019 13:30