a. Gross income = sales - COGS

Pretax = gross income - SG$A expense +operating income + non operating income- interest expense - unusual expense

income taxes = Pretax - net income

income statement 20162015201420132012

sale 5938755355558705270853341

COGS 2342520651205222141820507

gross earnings 3596234704353483129032834

SG&A EXPENSE 2114919835196931872918117

operating income 1481314869156551256114717

non operating income 533 -51 224 595463

interest expense 733 337 192 24490

unusual expense 1677269 -114 301 217

pretax 2774929081314562517229590

income taxes 1743317661197521555218585

Net income 103161142011704962011005

b. Average tax rate = total taxes / total taxable income ( for this calculation we need the tax table for identifying the correct tax brackets for each taxable income falling on it.

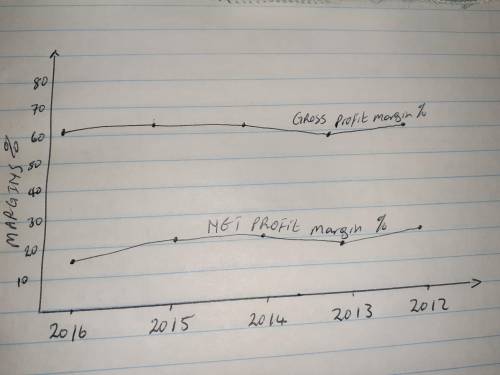

2016 2015 2014 2013 2012

gross profit margin 0.61% 0.63% 0.63% 0.59% 0.62%

net profit margin 0.17 % 0.21% 0.21% 0.18% 0.21

%

c. is attached

d.income statement 20162015201420132012

sale 100 100 100 100 100

COGS 39.44%37.31%36.73%40.64%38.45%

gross earnings 60.56%62.69%63.27%59.36%61.55%

SG&A EXPENSE 35.61%35.83%35.25%35.53%33.96%

operating income 24.94%26.86%28.02%23.83%27.59%

non operating expense 0.90%-0.09%0.40%1.13%0.87%

interest expense 1.23%0.61%0.34%0.46%0.17%

unusual expense 2.82%0.49%-0.20%0.57%0.41%

pretax 46.73%52.54%56.30%47.76%55.47%

income taxes 29.35%31.90%35.35%29.51%34.84%

Net income 17.37%20.63%20.95%18.25%20.63%

Explanation:

gross profit margin = gross profit/ sales

net profit margin = net profit / sales

no c is an attachment